US stocks were mixed on Tuesday with clear underperformance in the small-cap Russell 2000 - Newsquawk Asia-Pac Market Open

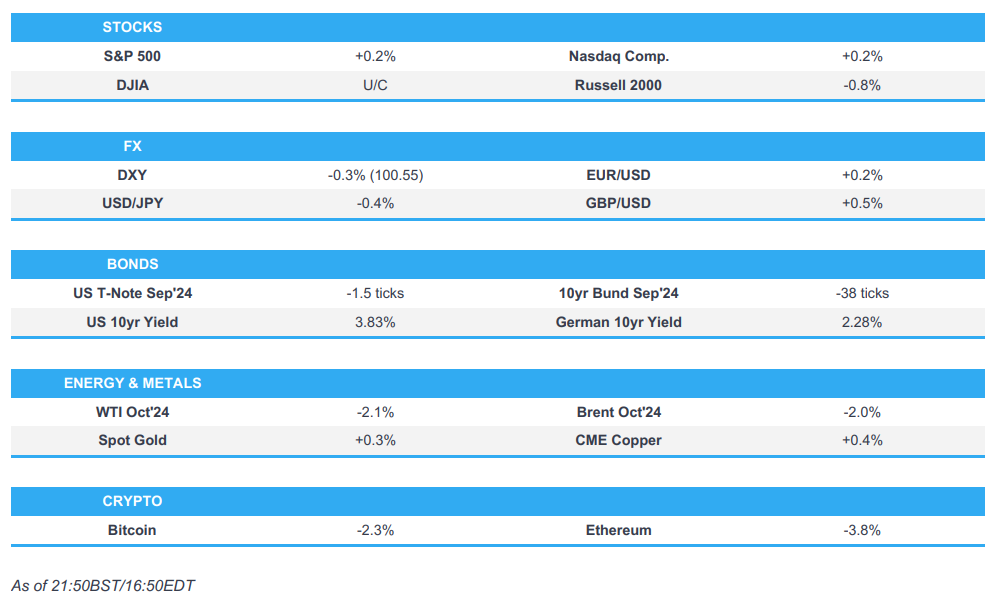

- US stocks were mixed on Tuesday with clear underperformance in the small-cap Russell 2000, in a day of thin headline newsflow as participants await tech behemoth Nvidia earnings on Wednesday after-hours.

- The Dollar was lower on Tuesday and retraced its gains seen on Monday, albeit in a week, so far, typical of summer trading conditions ahead of the Labour Day holiday next week.

- Light newsflow saw mixed price action in Treasuries, although settling off worst levels with the longer end seeing the greatest selling pressure.

- The crude complex almost wiped out Monday's gains, amid a lack of further geopolitical escalation, and participants' profit-taking.

- Looking ahead highlights include Australian AGB Auction, Australia CPI, BoJ's Himino, and Fed's Waller.

More Newsquawk in 2 steps:

1. Subscribe to the free premarket movers reports

2. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

SNAPSHOT

US TRADE

- US stocks were mixed on Tuesday with clear underperformance in the small-cap Russell 2000, in a day of thin headline newsflow as participants await tech behemoth Nvidia earnings on Wednesday after-hours.

- SPX +0.16% at 5,626, NDX +0.33% at 19,582, DJIA flat at 41,251, RUT -0.67% at 2,203

- Click here for a detailed summary.

NOTABLE HEADLINES

- US voters prefer Trump's approach to economy over Harris 43% to 40%, down from 11 point July lead - Reuters/Ipsos poll.

- Fed Discount Rate Meeting Minutes: Chicago and NY directors favoured a cut.

DATA

- US Redbook YY 5.0% (Prev. 4.9%)

- US Monthly Home Price YY (Jun) 5.1% (Prev. 5.7%, Rev. 5.9%)

- US CaseShiller 20 MM SA (Jun) 0.4% vs. Exp. 0.3% (Prev. 0.3%, Rev. 0.4%)

- US CaseShiller 20 YY NSA (Jun) 6.5% vs. Exp. 6.0% (Prev. 6.8%, Rev. 6.9%)

- US Consumer Confidence * (Aug) 103.3 vs. Exp. 100.7 (Prev. 100.3, Rev. 101.9)

- US Dallas Fed Services Revenues* (Aug) 8.7 (Prev. 7.7)

- US Texas Serv Sect Outlook* (Aug) -7.7 (Prev. -0.1)

FX

- The Dollar was lower on Tuesday and retraced its gains seen on Monday, albeit in a week, so far, typical of summer trading conditions ahead of the Labour Day holiday next week.

- G10 FX saw gains across the board, albeit to varying degrees, with the Kiwi outperforming and the Euro 'underperforming' on account of the weaker Dollar, as opposed to much currency-specific related.

- For the single currency, EUR/USD traded between 1.1151-90, with the German GDP and consumer sentiment data once again providing a bleak account for the region.

- In high beta FX, Cable saw a peak of 1.3265, while AUD/USD and NZD/USD saw highs of 0.6795 and 0.6254.

- The Yen initially saw weakness on Tuesday, with USD/JPY reaching a high of 145.17, but later retraced to lows of 143.93 on account of the aforementioned Buck weakness.

- EMFX was pretty mixed vs. the Dollar. The Yuan, TRY, and BRL were flat, while ZAR and RUB saw marginal strength, while the MXN was the distinct underperformer.

FIXED INCOME

- Light newsflow saw mixed price action in Treasuries, although settling off worst levels with the longer end seeing the greatest selling pressure.

- US sells USD 69bln of 2yr notes; stop-through 0.6bps. High Yield: 3.874% (prev. 4.434%, six-auction average 4.707%). WI: 3.880%. Tail: -0.6bps (prev. -2.3bps, six-auction avg. -0.2bps). Bid-to-Cover: 2.86x (prev. 2.81x, six-auction avg. 2.62x). Dealers: 11.9% (prev. 9.0%, six-auction avg. 13.7%). Directs: 19.1% (prev. 14.4%, six-auction avg. 20.1%). Indirects: 69% (prev. 76.6%, six-auction avg. 66.2%).

COMMODITIES

- The crude complex almost wiped out Monday's gains, amid a lack of geopolitical escalation, and participants' profit-taking.

- US Private Inventory Data (bbls): Crude -3.4mln (exp. -2.3mln), Distillate -1.4mln (exp. -1.1mln), Gasoline -1.9mln (exp. -1.6mln), Cushing -0.5mln

GEOPOLITICAL

- Russian Defence Ministry said Russia carried out a high-precision weapon strike on Ukraine overnight, via Interfax.

- Russian Deputy Foreign Minister said their response could be much tougher than earlier, via Ria; in the context of the Minister describing the US' involvement in Ukraine's Kursk incursion as "a fact".

- Ukraine President Zelenskiy said Ukraine has the next steps planned apart from the Kursk operation on the diplomatic and economic front; the plan is to be presented to US President Biden, Harris and likely Trump.

- An Israeli military source told Sky News Arabia "The army is ready for all options, including total war"; able to launch a pre-emptive strike at Iran, Syria, Lebanon or Yemen.

- Iran's Supreme Leader opens the door to nuclear negotiations and said no obstacles to dealing with America, but caution, according to Al Arabiya

- An Israeli delegation from the Mossad, the IDF and the Shin Bet will travel to Doha on Wednesday to continue talks with US, Qatari and Egyptian officials with the aim of closing the remaining gaps in the Gaza hostage and ceasefire deal, via Axios' Ravid.

- White House's Kirby said he believes Iran is "postured and poised" to launch an attack on Israel. Messaging to Iran has been "don't do it. There is no reason to potentially start some of regional war". US will defend Israel in the event of an Iranian attack. Still hopeful on Gaza ceasefire talks since all parties remain engaged.

CENTRAL BANKS

- ECB's Knot said excessive government spending has made it harder for the ECB to lower inflation; tighter government discipline is needed to make the new budget rules work, via Reuters. As long as the disinflation path converges to 2% before end-2025, then comfortable with gradual policy easing; will wait for data to decide September rate-cut view.

- ECB's Centeno said the path for interest rates seems relatively clear.

- CBRT Minutes: Leading indicators suggest that monthly inflation will slow down in August.

- Hungarian Hungary Base Rate (Aug) 6.75% vs. Exp. 6.75% (Prev. 6.75%). NBH said will make decisions on the level of the base rate in a cautious and data-driven manner. NBH Deputy Governor Virag said rate cuts have paused temporarily; further cautious rate easing possible.

EU/UK

NOTABLE HEADLINES

- UK PM Starmer said October budget will be "painful".

- Italian premier Meloni is reportedly looking to fill a EUR 12bln budget hole with measures such as cost cuts and delayed retirement, according to Bloomberg citing sources. Finance Minister Giorgetti has until Sept. 20 to deliver a fiscal plan to Brussels.

- Italy is to approve its updated fiscal plan by mid-September, according to The Treasury.

- EUROPEAN CLOSES: DAX: +0.44% at 18,698, FTSE 100: +0.21% at 8,345, CAC 40: -0.32% at 7,566, Euro Stoxx 50: flat at 4,897, AEX: flat at 908, IBEX 35: +0.55% at 11,327, FTSE MIB: +0.52% at 33,779, SMI: -0.55% at 12,291, PSI: +0.45% at 6,746

DATA

- UK CBI Distributive Trades (Aug) -27.0 (Prev. -43.0)

- German GDP Detailed QQ SA (Q2) -0.1% vs. Exp. -0.1% (Prev. -0.1%); YY SA 0.0% vs. Exp. -0.1% (Prev. -0.1%). YY NSA (Q2) 0.3% vs. Exp. 0.3% (Prev. 0.3%)Swedish PPI YY (Jul) -0.1% (Prev. 0.8%); MM -1.4% (Prev. -0.4%)

GLOBAL

- IDC sees worldwide smartphone shipments growing 5.8% Y/Y in 2024 to 1.23bln units. "The 12% growth in the first quarter, followed by 9% growth last quarter, has brought improved optimism about how 2024 will play out in the second half of the year."

Loading...